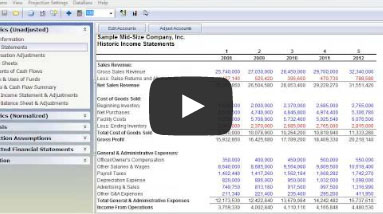

Financial statement data is necessary in order to analyze the current performance of the business and how that compares to past performance and its industry peers. Prior revenues, expenses and earnings provide a baseline for estimating future earnings and cash flows.

With BVS you can adjust any line-item in the historic income statement and balance sheet for any year. The purpose of normalization adjustments is to more accurately reflect the true economic benefits being valued. Financial statement adjustments are typically made to reflect items such as:

Explanatory notes can be added to document adjustments. BVS then prepares a set of Normalized Financial Statements including: Income Statements, Balance Sheets and Statements of Cash Flows along with:

A point of data by itself reveals very little information. However, when you have a point of data in relationship to other points of data over multiple time periods, a story begins to emerge. BVS gives you the information you need to analyze both the historic and normalized statement data and compare the results for up to 5 years to industry peers using either RMA Annual Statement Studies or Integra 5-Year Industry Reports.

The optional databases available from MoneySoft for industry peer comparisons are RMA Annual Statement Studies and Integra 5-Year Industry Reports.

The future earnings and dividend-paying capacity of a business are two of the elements required by Revenue Ruling 59-60. Further, the anticipated future performance of a business and the resulting benefit streams are a primary consideration of a buyer when contemplating the price they can or are willing to pay for a going concern.

Projected financial statements are needed when using discounted cash flow or discounted future earnings under the Income Approach. In addition, projected financial information is necessary when using the “first projected year” benefit streams under some of the methods in the Market Approach.

Projected financial information can be provided by management or developed by the analyst working with management. In many cases, you will find that management only provides projected profit and loss data, but not a balance sheet. So, it will be necessary to work with management to develop projected balance sheet data, which is needed prepare statements of cash flows along with an estimate of the other future benefit streams that will be considered in the valuation. In addition, balance sheet data is essential to analyze the adequacy of the firm’s capitalization and productive capacity.

In cases where management provides the projected income statements and accompanying balance sheets, it behooves the analyst test the information for mathematical coherence and reasonableness. By preparing projections, an analyst can compare the results to management’s projections and bring to light any issues that may require further action. Accepting management projections “right out of the box” is not a sound practice and an independent appraiser can not rely solely upon management’s assumptions.

With the above in mind, BVS allows you to prepare a comprehensive set of fully linked, line-item projections of the Income Statements, Balance Sheets, Statements of Cash Flows, Statements of Retained Earnings and Sources & Uses of Funds for up to 10 years. Projections for the first 2 years can be prepared on a monthly basis.

In addition to the projection options and reports mentioned above, BVS provides a review of the projected data using DuPont Analysis, Z-Score and the Sustainable Growth Rate method.

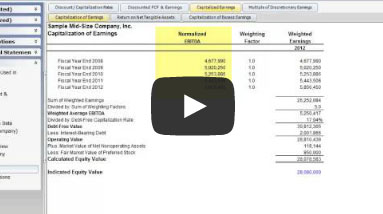

Data Summary: The financial statement data and benefit streams that are available in the valuation approaches and methods are restated and organized for historic and projected periods. Specific benefit streams for “Discretionary Earnings” are presented for the IBA Transaction Database as well as Pratt’s Stats and Done Deals.

Report Information: The data to be included in the business appraisal or valuation report is collected. Data points include:

Prior Transactions of Company Stock including a description, date, shares, class and transaction price. The prior transactions can be with related or third parties.

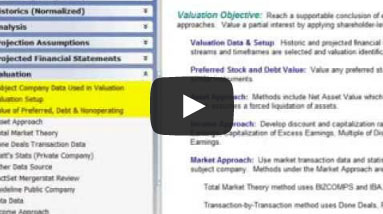

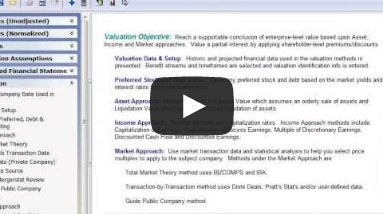

Valuation of Preferred Stock, Debt and Nonoperating Items: These are components that are used in the conversion of invested capital value to enterprise-level equity value and they can be adjusted to market in BVS:

The valuation approach based upon assets is sometimes referred to as the cost approach or replacement cost approach. The asset-based valuation methods included in BVS (Net Asset Value and Liquidation Value) are generally be considered to be minimum measures of business value. These methods do not consider the earnings capacity of a business. However, as minimum benchmarks of value, the business is generally worth at least Net Asset Value or Liquidation Value, even if the income, market, and other approaches yield lower values.

The Market Approach utilizes market prices of comparable companies to approximate the value of a company. In the valuation methods under the Market Approach, the price for a comparable company is expressed as a multiple of various measures of profitability and financial position. The price multiple from the comparable company is then applied to the respective measures of profitability and/or financial position of the subject company to determine the value of the subject company.

MoneySoft Business Valuation Specialist contains the following valuation methods under the Market Approach. The data sources along with the available multiples for each method are listed below. (Each method can include up to 100 records of transaction data):

Applying raw market and transaction data on an “as is basis” can provide misleading valuation indications. The application of market and transaction data in BVS for each of the databases utilizes the following procedures:

The Income Approach estimates value by considering the income (benefit streams) generated by the business over a period of time. This approach is based on the fundamental valuation principle that the value of a business is equal to the present worth of the future benefits of ownership.

The various business valuation approaches and methods provide different and sometimes conflicting indications of value. One of the primary duties of a valuation analyst is to review these value indications and reconcile them into a conclusion of value.

An independent and objective valuation eschews the notion of cherry-picking the value indications that support and favor the needs or bias of the client. Furthermore, before the values can be rationally reconciled, each value needs to be at the same level of value.

MoneySoft Business Valuation Specialist facilitates the selection of value and the reconciliation of selected value indications into a rational conclusion.

The software includes an iterative process that properly allocates the Adjusted Enterprise-Level Equity Value between voting and non-voting shares. Once the analyst selects an appropriate Premium for voting shares, the system will calculate the value for the voting and non-voting interests. The solution will be a per-share value for both groups that when multiplied by the total number of shares in that group and added together will equal the Adjusted Enterprise-Level Equity Value. The mere application of a Premium to arrive at the voting share value is an oversimplification and produces a result that does not total correctly.

The analysis includes a justification of the conclusion of Adjusted Enterprise-Level Equity Value. The justification is also referred to as a test of value, reality check or sanity check.

The justification of value is performed by structuring a hypothetical, arm’s-length purchase/sale transaction and then analyzing the estimated ROI to determine whether or not the returns are adequate to satisfy the hypothetical buyer.

The hypothetical terms and assumptions used in the justification of value as well as the metrics they yield are as follows:

The justification uses Adjusted Enterprise-Level Equity Value because the benefit streams that are used to evaluate reasonability are, in fact, Enterprise Level. To use Enterprise-Level benefit streams to evaluate a Shareholder (non-controlling) Level Value would tend to provide a false validation of reasonability.

The next step in the process is to convert Adjusted Enterprise-Level Equity Value to Shareholder-Level Value based upon a Partial Interest Percentage and/or Value Per Share. Shareholder-Level Value or Value Per Share can be determined for Voting or Non-Voting Shares. Dilution can also be applied to the Value Per Share. The process is described as follows:

- The amount of additional shares due to dilution is determined by comparing the Adjusted Enterprise-Level Equity Value Per Share to the exercise price for options and warrants to identify the number of shares that are in-the-money. In-the-money shares are considered exercised. A portion of the proceeds is applied toward the exercise price and the balance is considered additional shares. The additional shares are then added to the total shares outstanding along with any shares that would be issued for Convertible Preferred to arrive at the total outstanding shares on a diluted basis.

- Dilution is calculated separately for voting and non-voting, if any.

- The analyst selects whether voting or non-voting shares are being valued and whether dilution is included. The Percentage Interest to be Valued is selected and the Shareholder-Level Value Before Adjustments is presented.

- Adjustments (Premiums and Discounts) are then applied to the Shareholder-Level Value as a stated dollar amount or percentage. The number of shares in the partial interest (voting/non-voting with dilution, if any) is then divided into the Adjusted Shareholder-Level Value to determine the Value Per Share (a range may also be presented).

The supporting schedules provide all the details of the analysis and valuation. However this information usually needs to be summarized in the form of a written report for presentation to the client and other interested parties and authorities. The report builder streamlines the process of creating a professional and in-depth, text-based reports complete with the underlying assumptions and a description of the methods and procedures applied.

The Financial Report Builder links the numeric analysis with a structured valuation report narrative that automatically documents the analysis for you using Microsoft Word. The Financial Report Builder is “smart” enough to know what analysis you actually performed and describes the results of the analysis. Both the templates and generated reports are fully customizable using Microsoft Word.

If you’re looking for an equally serious valuation tool that will save you time and money preparing supportable and credible business valuations and appraisals, then you’ll want to try MoneySoft Business Valuation Specialist today!